The End of Easy Money

Reference

This article was originally published in Assiom Forex Letter No. 50 in Italian.

Market shift

For more than a decade, Europe’s financial markets operated under conditions that were anything but normal. The underlying machinery of markets disappeared beneath the surface, cushioned by abundant liquidity and policy support. Central bank intervention suppressed volatility, compressed sovereign yields and flooded the banking system with reserves.

Funding was ample, rates were extraordinarily low and, for a time, in many places, market discipline appeared suspended.

That illusion has now passed.

The return of inflation, geopolitical turmoil, renewed fiscal spending and tighter monetary policy have altered the landscape profoundly. Central banks have been dialing back their footprint in markets, sovereign issuance has risen, volatility has returned and liquidity once taken for granted now commands a price. In this more exposing environment, Asset Liability Management (ALM) has moved from being seen as a control function to becoming a strategic pillar of banking resilience.

Central banks step back

Covered bonds, asset-backed securities, sovereign debt and corporate bonds were all purchased at scale. During the pandemic period, the Pandemic Emergency Purchase Programme (PEPP) added further momentum [CS2.1][JC2.2]and flexibility. Banks, meanwhile, benefited from targeted longer-term refinancing operations that provided attractive funding supporting their continued lending to the real economy.

The combined effect was straightforward. The ECB absorbed large volumes of securities while supplying reserves to the banking system. Liquidity became abundant, funding conditions eased sharply and the need for banks to rely on private money markets diminished. Repo remained essential to market structure, but for many institutions its urgency faded.

From 2022 onwards, however, the cycle turned. Inflation surged, energy prices spiked (catalysed by the Russian annexation of Crimea), leading to cost-push inflation compounded by supply chain disruptions. Policy priorities shifted rapidly. Net purchases ended, refinancing programmes were recalibrated, targeted longer-term refinancing (TLTR) operations were allowed to run out, and interest rates were engineered upwards. Quantitative tightening (QT) began, with a gradual shrinking of the Eurosystem balance sheet and a greater share of intermediation returning to private markets.

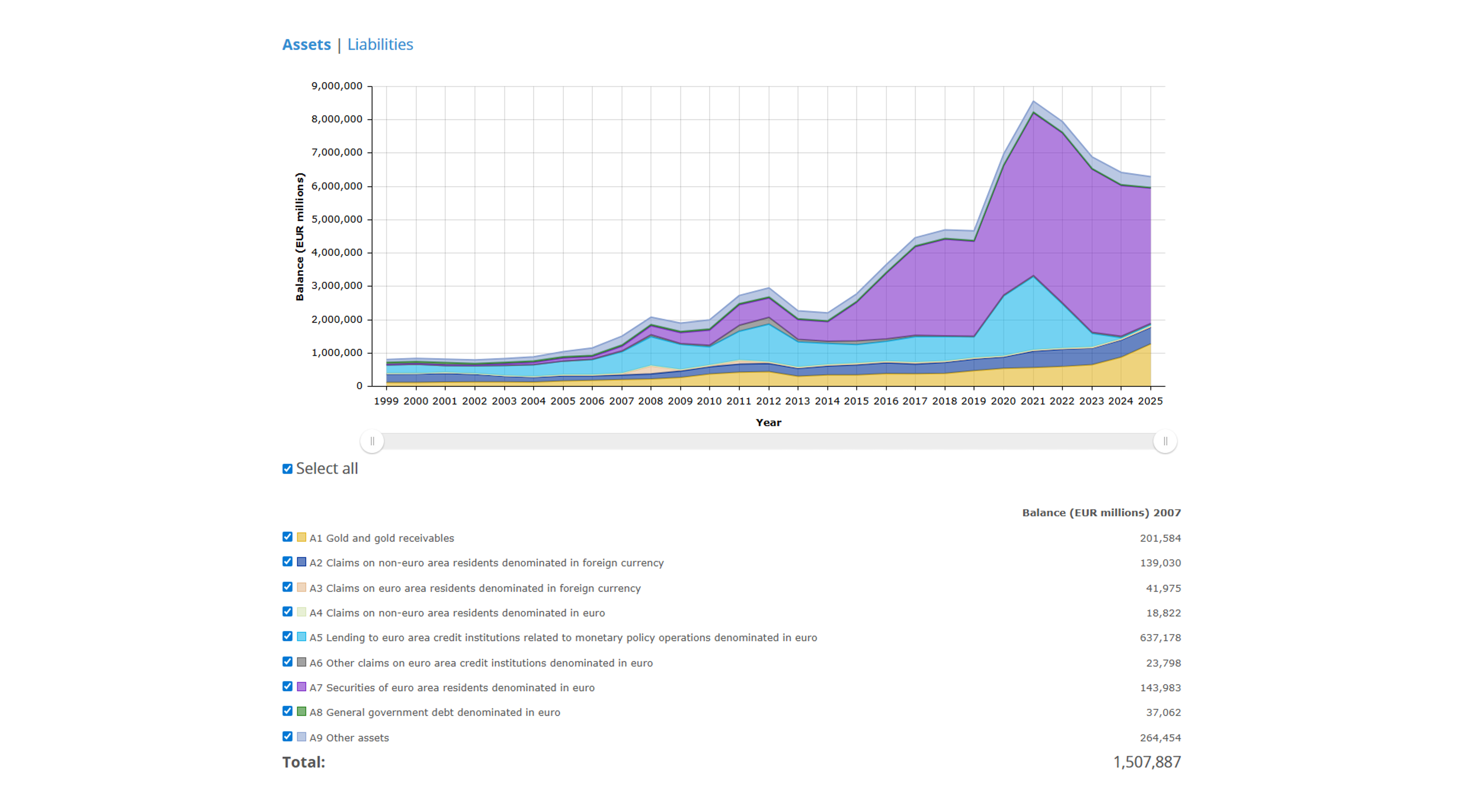

See below chart showing the evolution of the ECB’s balance sheet.

Source: Annual consolidated balance sheet of the Eurosystem

Few markets better illustrate this transition than the repo market.

Repo, often described as the plumbing of modern finance, is in truth one of its central arteries. It allows institutions to borrow cash against securities, finance inventories, mobilise collateral and distribute liquidity efficiently across the system.

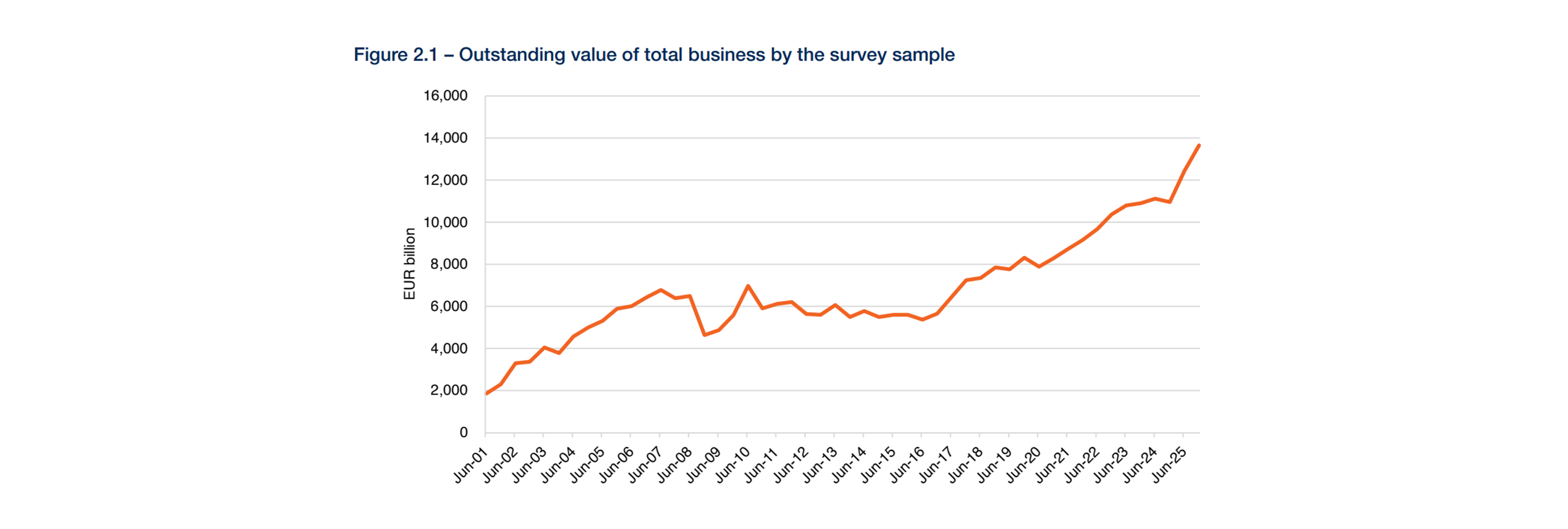

During the quantitative easing (QE) years, excess reserves reduced the need for many banks to seek short-term funding in private markets. As reserves declined under QT, the opposite occurred. Banks increasingly returned to secured funding markets, while buy-side institutions and corporates became more active providers and distributors of liquidity. The same was true for many public sector entities, who in some cases saw the end to remuneration of the balances held at their respective central banks, bringing repo as a liquidity management tool back into focus. The International Capital Market Association’s (ICMA) latest survey shows significant growth in the repo market in recent years, reaching over €13.6 trillion at the end of 2025.

At the same time, rates, previously closely anchored to the ECB deposit facility became more differentiated. Collateral quality, scarcity, tenor and balance sheet demand mattered again. In short, money regained its market price.

The expansion of the European repo market in recent years reflects this structural change. It has re-emerged not just as a funding tool, but as a core mechanism through which sovereign debt is financed, collateral is transformed, and liquidity is redistributed throughout the system.

See below chart showing the evolution of the repo market.

Source: ICMA European Repo Market Survey

This return to market discipline has, however, not taken place in calm conditions.

The pandemic, the European energy crisis, the UK gilt episode, banking sector stresses in 2023, trade tensions and broader geopolitical uncertainty have all triggered bouts of sharp volatility. These episodes serve as reminders that liquidity conditions can tighten abruptly when confidence falters.

For ALM and treasury professionals, volatility changes everything. Margin calls rise, collateral demands increase, and institutions must have immediate access to high-quality liquid assets (HQLA). Liquidity buffers that appear ample in benign conditions can prove less comfortable under stress.

Treasury functions today must therefore operate with a far greater degree of agility than was required during the years of abundant central bank liquidity.

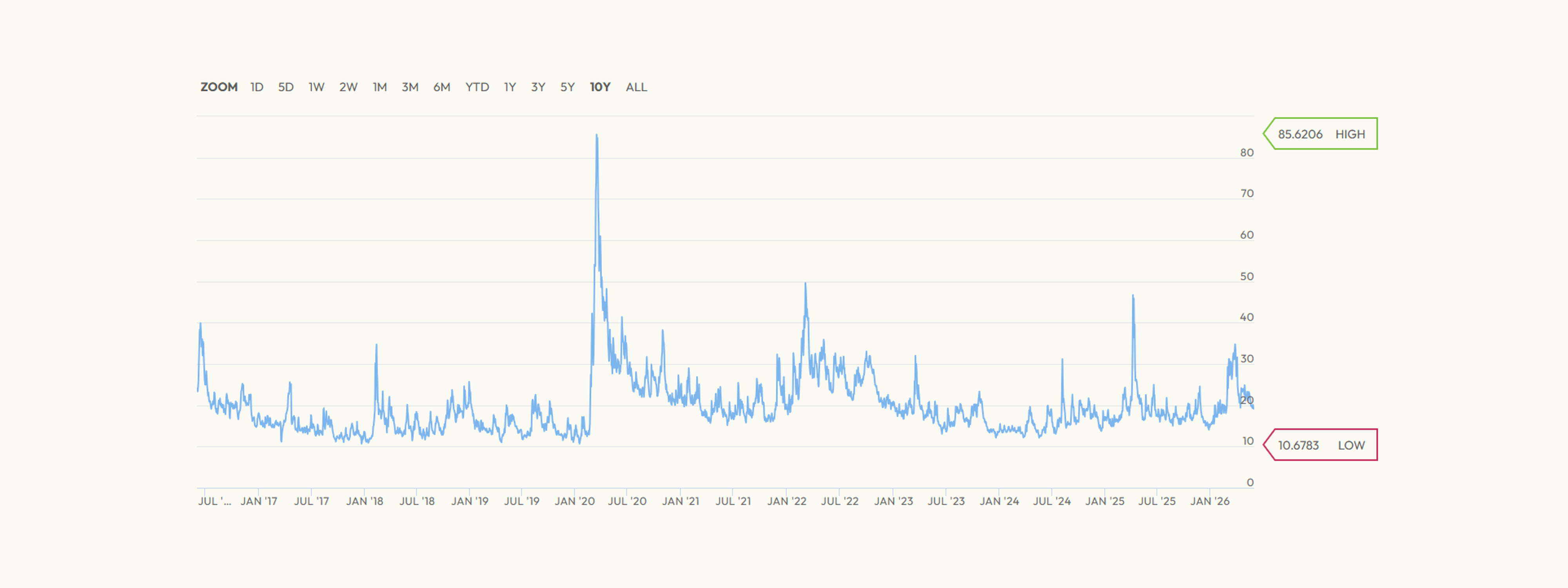

See below chart showing market volatility.

Source: EURO STOXX 50® Volatility (VSTOXX®) - STOXX

Capital, liquidity, discipline

Concurrently, European governments have faced mounting expenditure demands. Pandemic support measures were followed by energy subsidies, defense spending, industrial policy initiatives and the broader fiscal consequences of slower growth and demographic pressure.

The result has been higher public borrowing needs across much of the continent. Sovereign debt burdens remain manageable in many jurisdictions, but clearly elevated relative to the pre-crisis era.

The significance for markets was that government financing needs were rising just as official central bank demand had diminished.

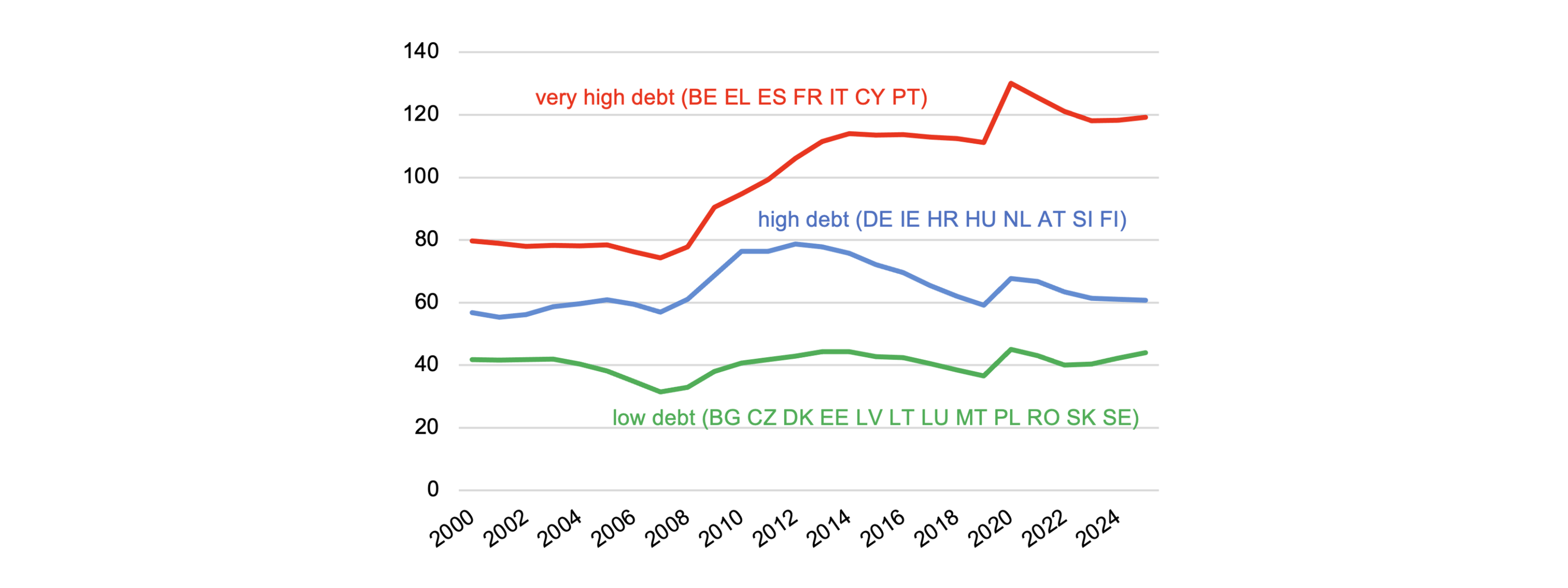

See below chart showing the rise in government debt-to-GDP.

Source: High government debt in the EU or the end of ‘enjoy now, pay later’ | CEPR

This increased spending, combined with central banks no longer being the primary buyers of government debt, has meant new bond issuance must be absorbed by the private market (banks, pension funds, asset managers, etc.). This puts upward pressure on sovereign yields: a fact particularly relevant in any ALM and risk management function and one that has adversely impacted bond valuations.

As banks increase their holdings of domestic and European government bonds, the health of their balance sheet becomes more tightly linked to that of the sovereign. Sovereign bonds remain important liquidity assets and collateral instruments, yet larger holdings must be funded, hedged and managed in a world of higher rates. The relationship between sovereign risk and banking sector resilience therefore remains highly relevant albeit evolved in form.

Alongside these macroeconomic challenges, regulation continues to shape balance sheet decisions.

Temporary relief measures introduced during the pandemic have largely expired. Final Basel III implementation is progressing, while leverage ratio, capital and liquidity requirements remain central supervisory priorities.

Europe’s planned move toward T+1 settlement adds another layer of complexity. Reducing the settlement cycle from two days to one compresses the time available to source securities, arrange financing, execute foreign exchange and resolve operational breaks.

What may appear an operational adjustment is, in reality, a meaningful treasury challenge. Intraday liquidity access and management, forecasting precision and straight-through processing will become even more valuable.

The current ALM function is no longer a passive custodian of liquidity. It is an active manager of competing constraints.

ALM teams must preserve resilience while supporting profitability. They must hold sufficient liquidity buffers whilst limiting drag on returns (HQLA are typically low-yielding assets). They must support the business whilst at the same time respecting the leverage constraints which act as a hard cap on the institution’s balance sheet size, making every transaction's return on assets critical.

Examples of banks worldwide failing on the ALM side (Silicon Valley, First Republic, Signature Bank) serve as vivid reminders of the importance of sound and resilient treasury and ALM management, and both functions are increasingly strategic and visible within complex financial organizations.

As previously mentioned, the banking system is more than ever asked to absorb higher volumes of debt issuance. In turn, banks must secure their refinancing in the markets. And they are forced to do this in the labyrinth of regulatory measures such as the Liquidity Coverage Ratio (LCR), Net Stable Funding Ratio (NSFR) and Leverage Ratio. During the QE era, abundant reserves made these metrics easier to manage. Today, optimisation is materially more complex.

Every use of balance sheet counts as an opportunity cost.

New tools, new markets

Repo has proven to be a crucial tool for market participants in allowing them to manage liquidity and risks and has been interlinked with fixed income markets and issuance for decades. The importance of the tool is highlighted further by current market conditions.

Repo allows institutions to raise funding against securities holdings, improve liquidity profiles, optimise collateral usage and manage short-term (under 3 months) balance sheet needs. Depending on collateral type, maturity and structure, repo transactions can materially influence liquidity ratios and funding costs.

For institutions rich in lower-yielding liquidity assets, repo can also be a means of enhancing returns. For others, it offers access to secured funding at scale and at speed.

Provided the trade is relevant in terms of duration for the LCR calculation, repo can be a tool for treasurers to lend cash and monetize excess LCR ratios (when taking lower-quality collateral that still fit their policy i.e. downgrade trade). For instance, lending cash (level 1) versus LCR 2b collateral will lower the LCR ratio of the cash lender temporarily but will attract a higher interest rate on the cash lent than if the collateral was LCR 1. Equally, for banks seeking funding and LCR ratio improvements, repo can be a way to upgrade their LCR by borrowing cash versus lower-LCR-level collateral or even non-HQLA. The high flexibility of repo and the depth of the market bring broad opportunities for those involved.

Equally important is the diversity of counterparties now active in the market. Corporates, sovereign agencies, ministries of finance (who bring an NSFR ratio benefit to the bank counterpart that borrows cash from them), and buy-side institutions all contribute to a broader and more resilient ecosystem. Access to deep, diversified liquidity, both cleared and bilateral, has become a strategically valuable aspect of the repo market.

Collateral has become one of the defining strategic resources of modern banking.

Institutions increasingly seek to manage securities inventories holistically across repo, derivatives margining, securities lending and central bank facilities. The objective is to allocate the cheapest eligible asset to each need while preserving scarce high-quality collateral for periods of stress and monetisation.

This requires sophisticated systems that enable market participants to visualize and mobilize inventory across the capital markets ecosystem, strong operational discipline and reliable market infrastructure. Triparty arrangements, (which have seen massive growth in recent years), central clearing connectivity and real-time inventory management tools such as those offered by Deutsche Börse Group are increasingly important. Altogether, the goal is to facilitate high straight-through-processing rates from trading to timely settlement and automated collateral management.

The Eurosystem Collateral Management System, developed across the Eurosystem and now also connected to the post-trade triparty systems, is also significant in this regard. By harmonising collateral mobilisation processes, it strengthens the ability of banks to access home central bank liquidity efficiently when and where it’s needed. Many institutions rightly regard this as an important and strategic resilience tool in a fast-moving world.

Another defining feature of current market dynamics is that interest in cleared repo continues to grow alongside bilateral markets, as institutions seek netting benefits, operational efficiency and reduced counterparty exposure. Repo markets continue to diversify and now include, in addition to banks, neo-brokers, challenger banks, ministries of finance, debt management offices, agencies, supranationals, corporate treasuries, insurance companies, pension funds, asset managers, wealth managers etc.

Longer-dated secured financing for credit assets is also expanding as banks seek more stable refinancing structures for corporate and structured bond holdings, (released back to the market by the ECB with the introduction of QT). The increasing involvement of structurers at banks in such transactions shows how the longer-term ratio management of a bank is linked with the refinancing of these assets.

From siloed balance sheet management toward cross-asset optimization

Perhaps most importantly, firms are moving away from siloed balance sheet management toward cross-asset optimization. Bonds, equities, funds and cash are increasingly viewed as components of one collateral pool to be deployed intelligently across multiple obligations.

One of the clearest lessons of recent years is that concentration is dangerous. Banks have therefore diversified funding sources beyond central bank facilities through greater use of repo, covered bonds, senior issuance, securitisation and ESG-linked instruments.

Diversification applies equally to counterparties, collateral pools, currencies and operational channels and strategic partners. Institutions that rely on a narrow set of funding avenues often discover their weakness at precisely the wrong moment.

Robust funding practices are no longer merely prudent. They are essential.

Technology is becoming increasingly central to treasury and ALM effectiveness.

Real-time liquidity dashboards, automated collateral engines, predictive analytics and seamless connectivity to infrastructures all improve responsiveness and control.

Tokenisation may, over time, offer further benefits through faster settlement, improved collateral mobility and greater transparency. The European Union’s DLT initiatives and work around digital money, including the digital euro, suggest that this direction of travel should be taken seriously.

Technology alone, however, is never enough. Strong governance, clear risk ownership and disciplined execution remain decisive.

Resilience as advantage

The new European ALM landscape is fundamentally different from that of the QE era.

Liquidity is no longer abundant by default. Sovereign supply is larger. Markets are more volatile. Regulation is more demanding. Balance sheet is scarcer and therefore more valuable.

In such an environment, sound ALM becomes a strategic differentiator.

The institutions best placed for the years ahead are likely to be those that combine disciplined governance, diversified funding, deep market access and the modern collateral infrastructure that will allow them to respond calmly during periods of stress.

Europe has moved from a world defined by sovereign support to one increasingly shaped by banking resilience.

At the centre of that transition sits ALM.