Investment funds (Depositaries) - Switzerland - CFCL

Reference

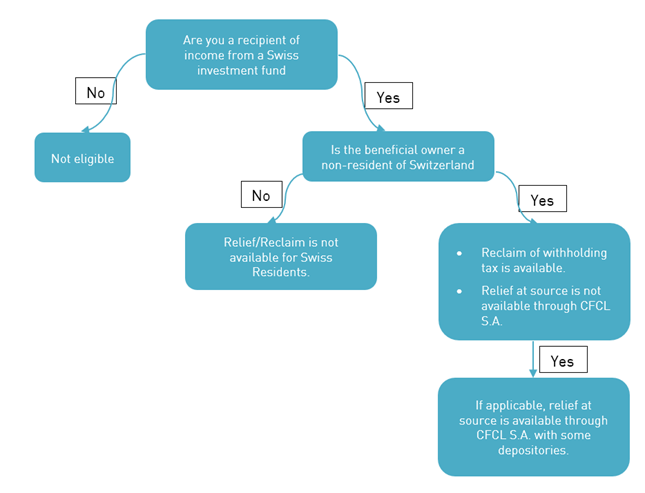

Who can obtain relief through Clearstream Fund Centre?

Summary of relief available

The standard rate of withholding tax on income payments on Swiss investment funds is 35%.

Beneficial owners' eligibility for relief

Beneficial owners' eligibility for relief is as follows:

Non-residents of Switzerland

A reclaim of withholding tax is available through Clearstream Fund Centre if:

- More than 80% of the income from the Swiss investment fund is derived from a foreign source;

and - The beneficial owner qualifies as a non-resident of Switzerland.

The client can reclaim withholding tax on behalf of the beneficial owner through Clearstream Fund Centre by submitting the appropriate documentation, if offered by the Depository.

If applicable, Relief at source from withholding tax on income payments from Swiss investment funds is available through Clearstream Fund Centre with some Depositories. In case of Tax Reclaim availability Clearstream will notify its clients via Swift message qualifier WTRC.

The position which is not disclosed as affidavit eligible will be considered by Clearstream Fund Center agent as being held by Swiss residents and will be subject to the maximum default rate applicable. This position will also be eligible to the additional distribution applicable to Swiss residents, if any.

Statutory deadline

The statutory deadline for reclaiming withholding tax is three years after the end of the calendar year in which the income is paid.

Acceptance of tax requests is dependent on each Depository, therefore, Clearstream can only support requests that strictly adhere to deadlines mentioned in the tax notifications released to its clients for each event.

Any reclaim request received after such period will be handled on a best effort basis with no result guaranteed and subject to approval by the Depository.

With respect to tax reclaims in general, clients are reminded that Clearstream Fund Centre accepts no responsibility for their acceptance or non-acceptance by the paying agent or the tax authorities of the respective country. It is the client’s responsibility to determine any entitlement to a refund of tax withheld, submit Bank Declaration (Affidavit) correctly, and to calculate the amount due.

Obtaining relief at source from withholding tax

Who can obtain relief at source?

If applicable, Relief at source from withholding tax on income payments from Swiss investment funds is available through Clearstream Fund Centre with some Depositories. In case of Tax Reclaim availability Clearstream will notify its clients via Swift message qualifier WTRC.

Reclaiming withholding tax

Tax reclaim - Who can reclaim withholding tax?

Beneficial owners can reclaim withholding tax on income payments from Swiss investment funds as follows:

Eligible Recipients | Effective rate of tax after refunda | Tax refund availablea |

Beneficial owners not resident in Switzerland | 0% | 35%b |

a. Expressed as a percentage of the gross income.

b. The tax refund is 35% when the amount of the distribution per unit initially paid equals the amount indicated in the bank declaration. Clients should note that if these amounts are different, the tax refund may be less than 35%.

Tax reclaim - What documents are required?

To reclaim withholding tax on income payments, the following must be submitted to Clearstream Fund Centre:

Bank Declaration |

Bank Declaration (Affidavit) |

A Bank Declaration (Affidavit) is required for each income payment for each investment fund in order to reclaim withholding tax on income payments. Bank Declaration (Affidavit) must be submitted to Clearstream via formatted message MT565 / Free-formatted message MT568/599 for each payment and not via original/paper document.

Clearstream Fund Centre will send a tax notification to each client receiving an income payment from a Swiss investment fund with the text of the Bank Declaration (Affidavit), that the Clearstream Fund Centre client, being a designated bank, must comply where necessary and submit to Clearstream Fund Centre via formatted message MT565 / Free-formatted message MT568/599 for each payment.

Clients may face a currency risk and delay in receiving the refund, if the affidavit declarations are not submitted by the required deadline mentioned in Clearstream Fund Centre notification for guaranteed exemption at source when applicable. Clients who do not submit Bank Declaration (Affidavit) prior to the deadline may receive the Swiss anticipatory tax refund in CHF, as opposed to the original currency. Furthermore, there may be a delay in receiving the refund. The decision as to whether the refund will be paid in the original currency or in CHF, will be at the discretion of the paying agent. Paying agents must pay the Anticipatory Tax to the Swiss Federal Tax Authority (FTA) in CHF and therefore, can only reclaim CHF from the FTA. The fact that the paying agent has to reclaim the Swiss anticipatory tax from the FTA, can also lead to delays in receiving the refund.

In the declaration the client certifies that:

- The legal title to the income belonged to non-residents of Switzerland;

- It was holding the investment fund shares for safekeeping on behalf of the beneficial owners on the date of the payment and has credited their accounts with the income; and

- It will at any time upon request submit supporting documentation (pièces justificatives).

Correspondingly, the Swiss bank paying the income from Swiss investment funds requests its clients to provide a similar Bank Declaration (Affidavit).

The text of the Bank Declaration (Affidavit) is specified in each tax notification released by Clearstream to its clients.

Who completes it? | Client. |

How often is it provided? | Per income payment. |

When is it provided? | Within Clearstream deadline as per tax notification |

How is it provided? | Formatted message MT565 / Free-formatted message MT568/599 |

Tax reclaim - What is the deadline for receipt of Bank Declaration (Affidavit)?

The statutory deadline for reclaiming withholding tax is three years after the end of the calendar year in which the income is paid.

The deadline by which Clearstream Fund Centre must receive the bank declaration is, specified on the tax notification. All bank declarations received after this deadline will be processed by Clearstream Fund Centre on a “best efforts” basis. However, in such cases, Clearstream Fund Centre accepts no responsibility for Instructions that have not reached the paying agent by the deadline.

With respect to tax reclaims in general, clients are reminded that Clearstream Fund Centre accepts no responsibility for their acceptance or non-acceptance by the paying agent or the tax authorities of the respective country. It is the client's responsibility to determine any entitlement to a refund of tax withheld, to complete the Bank Declarations (Affidavit) required correctly, and to calculate the amount due.

Tax reclaim - When are refunds received?

The estimated time for receiving a refund is depending on the upstream Depository and may take up to several months.