Guide on completing the Application for Entitlement to Reduced Tax Rate on Domestic Source Income (for Foreign Corporation) [Form No.72-2]

Applicant

If the corporation holds an Investment Registration Certificate (IRC), the name indicated in the IRC field must be the same name as mentioned in the IRC. If a beneficial owner who is a corporation receives Korean source income indirectly through an Overseas Investment Vehicle (OIV), such beneficial owner should submit this application form to the OIV rather than directly to Clearstream Banking. Please do not use any initials as it must be provided in the full name of the applicant.

Type of entity - Corporation

If the Applicant is a manufacturing company, bank, financial company, or other incorporated as a company who is the actual beneficial owner of the Korean income, then in general the Applicant would select “corporation” as beneficial owner on the Application for Entitlement to Reduced Tax Rate on Domestic Source Income (for Foreign Corporation) [Form No. 72-2], item 1.

{kind=link}

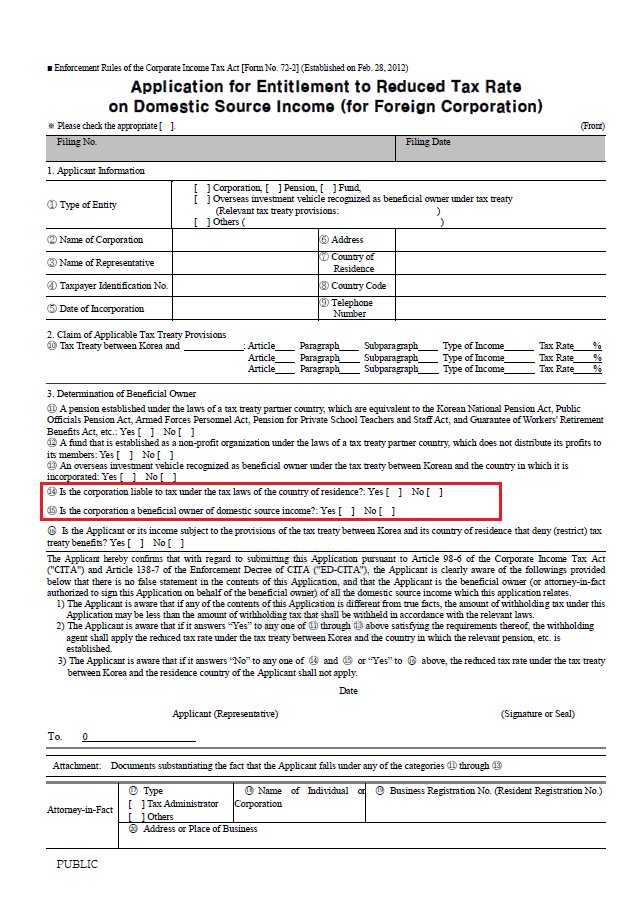

In order to declare if it is the beneficial owner of the income, it is required to answer “Yes” to the questions 14 and 15 on the Application for Entitlement to Reduced Tax Rate on Domestic Source Income (for Foreign Corporation) [Form No. 72-2], No.3 Determination of BO, items 14 and 15.

{kind=link}

The questions are as follows:

- 14. Is the corporation liable to tax under the tax law of the country of residence?

- 15. Is the corporation a beneficial owner of domestic source income?

If the Applicant answers “No”, to either one of above, the Applicant will be considered ineligible for treaty benefits and therefore subject to the default tax rate, except for the entities deemed as beneficial owner.

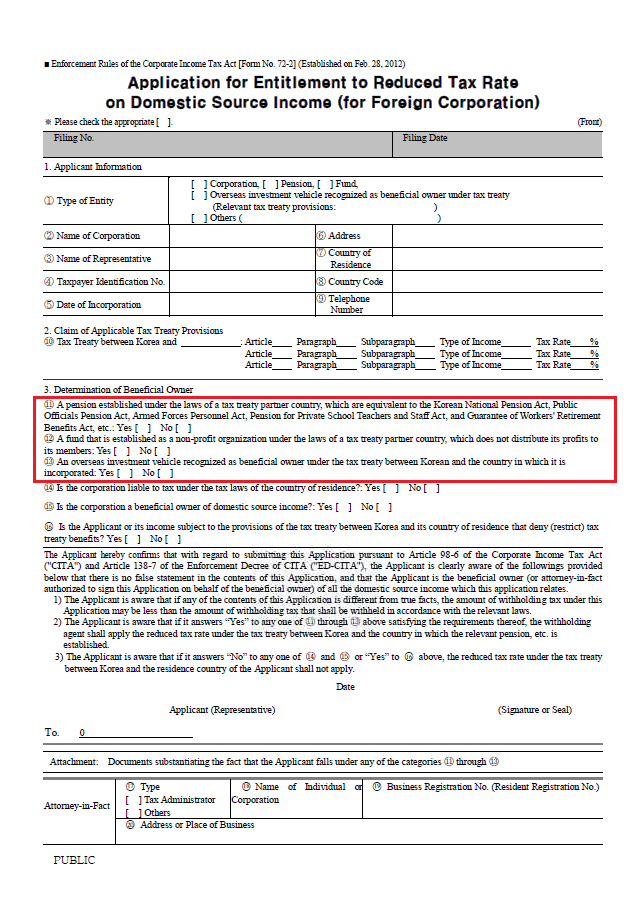

Type of entity deemed as beneficial owner (Pension, Non-profit Fund)

The below entities could be deemed as beneficial owner, when the Applicant answers “Yes” to one of the questions 11 or 13 on the Application for Entitlement to Reduced Tax Rate on Domestic Source Income (for Foreign Corporation) [Form No. 72-2], No.3 Determination of BO, items 11 and 13. These entities have to provide the necessary documents to prove their status and the applicable treaty rate.

{kind=link}

As an exception, if the Applicant answers “Yes” to either one of the questions 11 or 13, then it is possible to answer “No” to the above questions 14 and 15.

- 11. A pension established under the laws of a tax treaty partner country which are equivalent to the Korean National Pension Act, Public Officials Pension Act, Pension for Private School Teachers and Staff Act and the Guarantee of Workers’ Retirement Benefits Act, etc.

- 12. A fund that is established as a non-profit organisation under the laws of a tax treaty partner country, which does not distribute its profits to its members.

- 13. An OIV recognised as beneficial owner stated under the treaty.

In such cases, additional evidential documents are required to be attached to the form. The evidential documents should be substantiating that the Applicant falls under any of the above categories, however, there is no detailed guideline on what kind of evidential form is required.

The legislation in each country where there is a double taxation treaty with Korea may vary and in the event of any doubt, we recommend that foreign investors should consult their own tax advisors.

For the further information, please refer to the below;

- A pension: Customers, who wish to refer to an English version of the Korean National Pension Act, please refer to the National Pension Service website: However, English translated laws on the Public Officials Pension Act, Pension for Private School Teachers and Staff Act and the Guarantee of Workers’ Retirement Benefits are not available at this stage.

- A non-profit fund: According to the Korea Tax Authority, evidence of these non-profit entities can be proven via an annual income tax report filled in by the non-profit entity; for example, charities would normally claim exemption from tax via these tax statements. For private funds established by private corporations, they should not choose this type of beneficial owner, but they should instead complete the Report of Overseas Investment Vehicle plus the Schedule of Beneficial Owners.

- OIV recognised as beneficial owner under the tax treaty: As of today, none of the existing treaties specifically recognised OIV as the beneficial owner. For the updated treaties, please refer to the NTS website.

Type of entity - Other

If the Applicant is a central bank, central and/or municipal government, or other then please select “others” and describe the type accordingly on Application for Entitlement to Reduced Tax Rate on Domestic Source Income (for Foreign Corporation) [Form No. 72-2], item 1.

{kind=link}

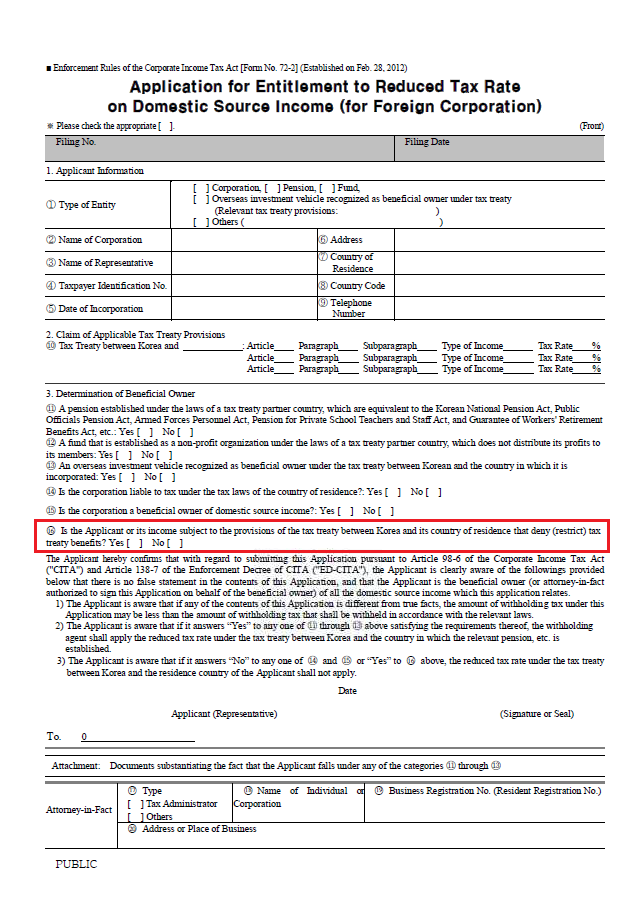

The question is as follows:

- 16. Is the Applicant or its income subject to the provisions of the tax treaty between Korea and its country of residence that deny (restrict) tax treaty benefits?

If the existing treaty specifically denies treaty benefits, the Applicant shall not enjoy the reduced tax rate, for example, Article 17 of Tax Treaty between Korean and U.S.A, or Article 1 of second protocol of Tax treaty between Korea and China.