Guidance for the use and completion of tax forms for debt securities and equities - South Korea

The forms required to be completed and submitted by beneficial owners investing in South Korean securities on their own behalf vary depending on the status of the respective final beneficial owner.

More detailed guidance regarding the completion of specific tax forms can be found as follows:

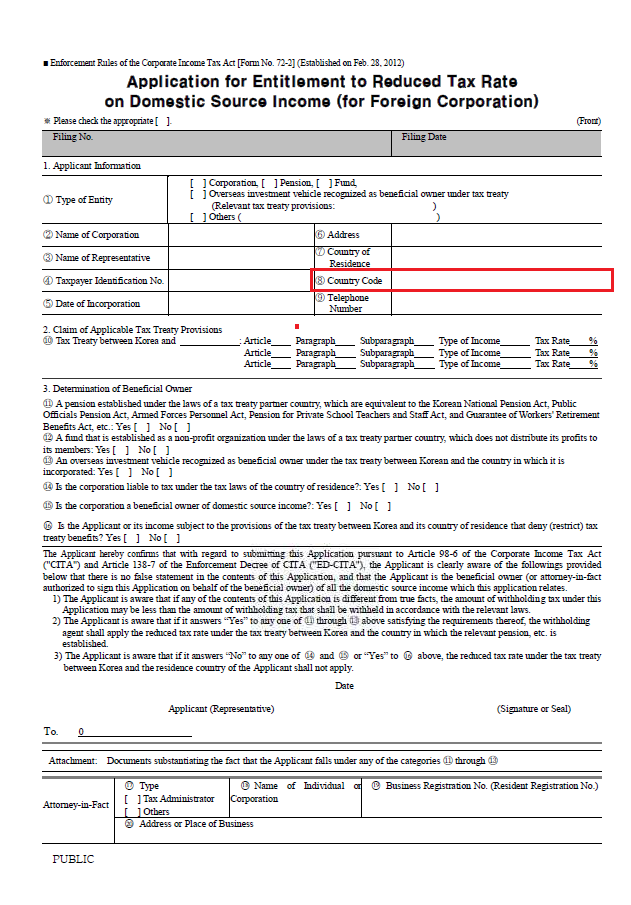

- Guide on completing the Application for Entitlement to Reduced Tax Rate on Domestic Source Income (for Foreign Corporation) [Form No.72-2]

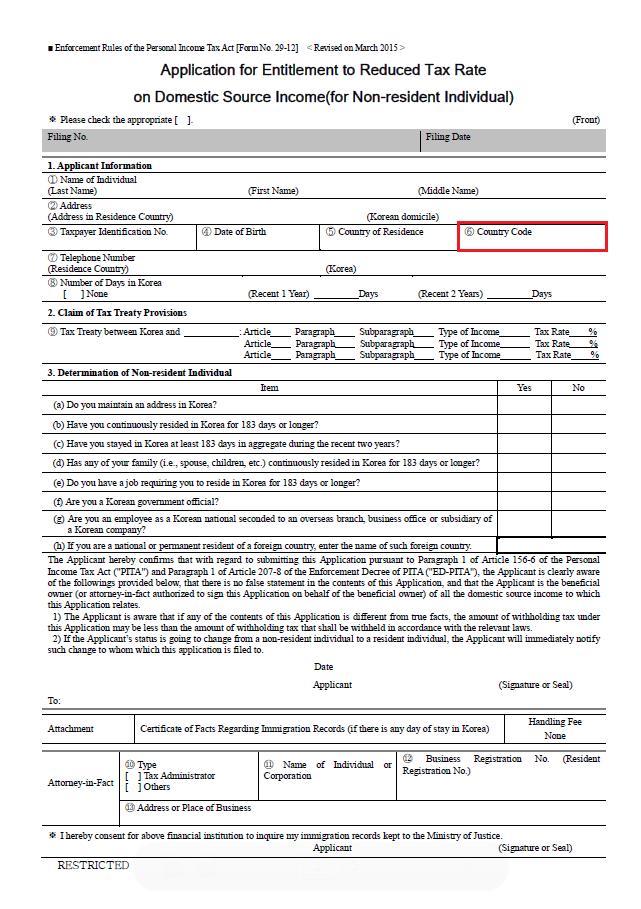

- Guide on completing the Application for Entitlement to Reduced Tax Rate on Domestic Source Income (for Non-resident Individual) [Form No.29-12]

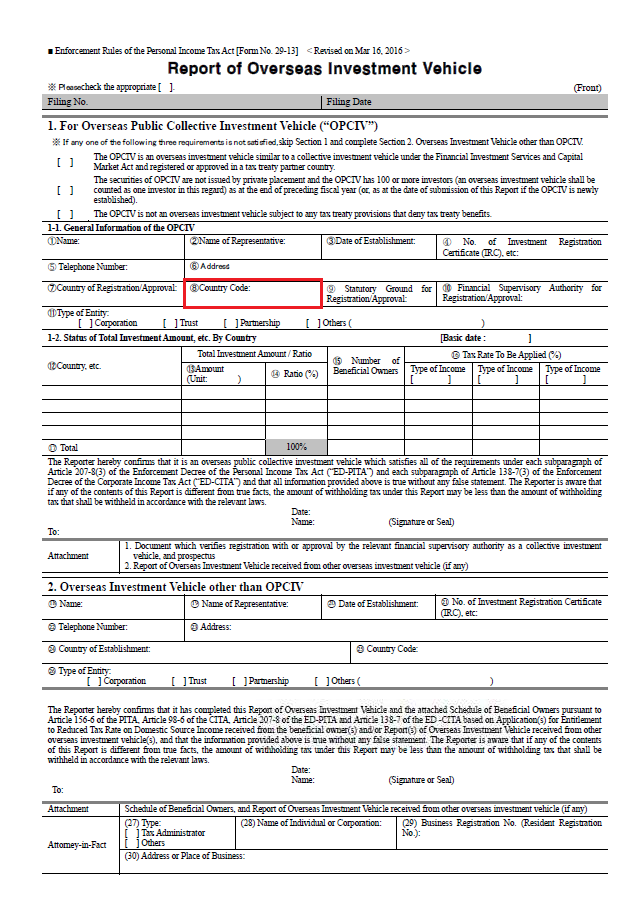

- Guide on completing the Report of Overseas Investment Vehicle (OIV) [Form No.29-13]

- Guide on completing the Schedule of Beneficial Owner [Annex to Form No.29-13]

General guidance for the use and completion of tax forms

Information of tax treaties

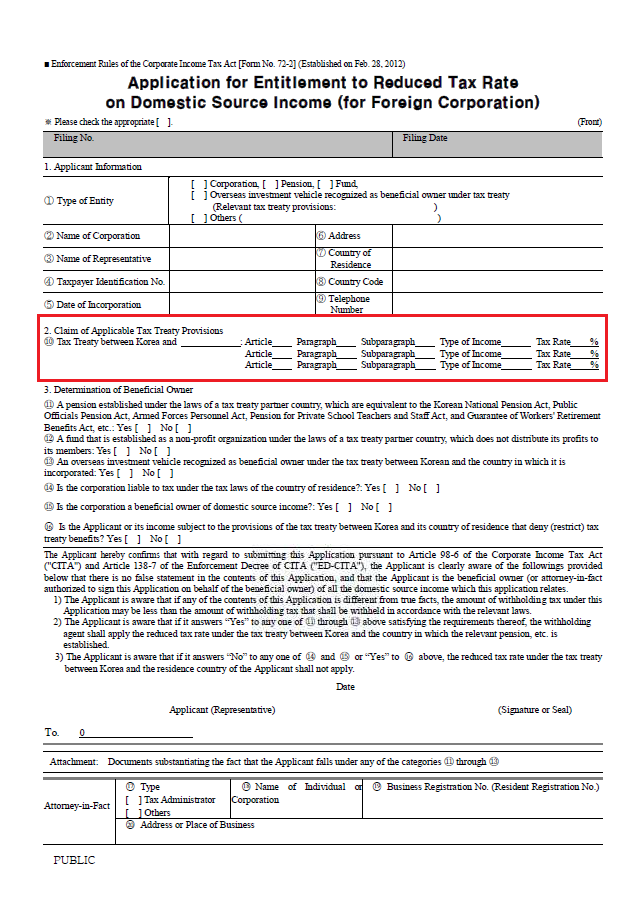

- Application for Entitlement to Reduced Tax Rate on Domestic Source Income (for Foreign Corporation), item 10;

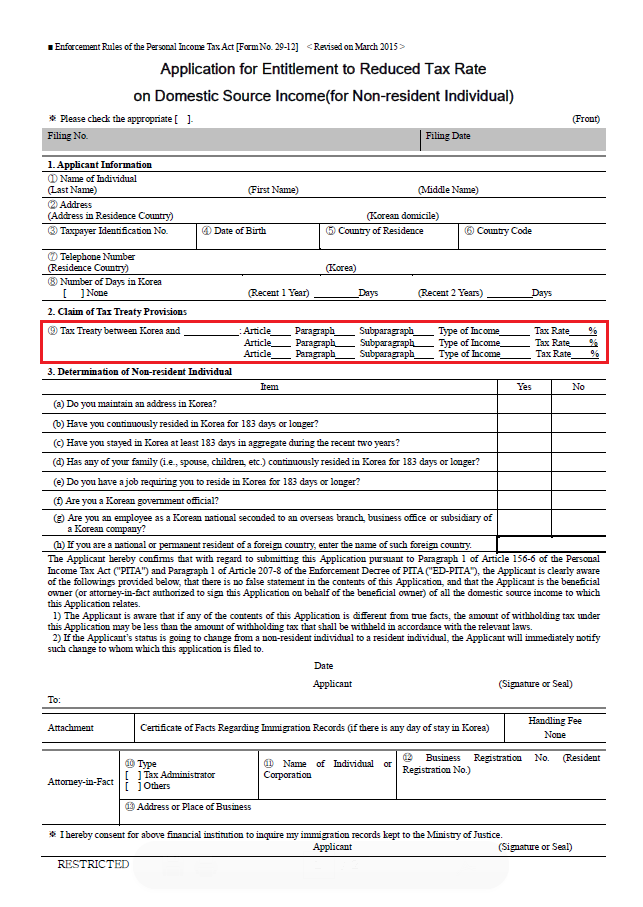

- Application for Entitlement to Reduced Tax Rate on Domestic Source Income (for Non-resident Individual), item 9;

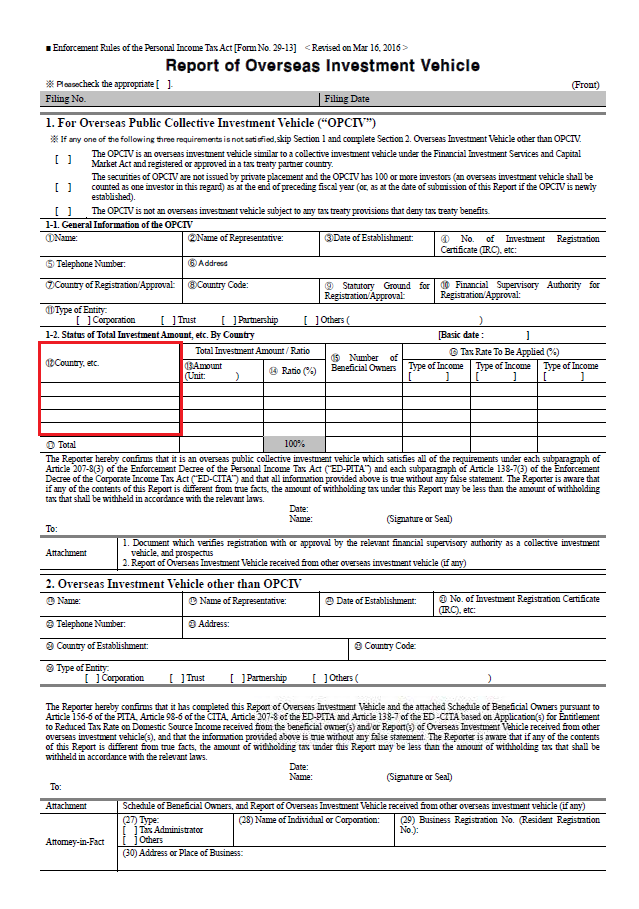

- Report of OIV, item 12;

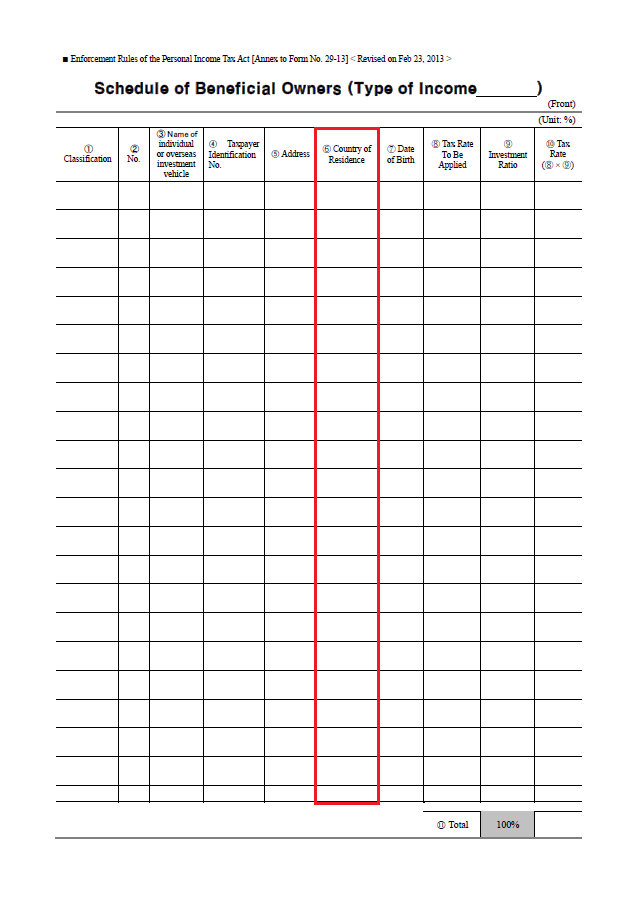

- Schedule of BO, item 6.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

On the above forms and for the mentioned items, please specify the country of tax residence of the Applicant. Additionally, in the spaces provided, please quote the article, paragraph, subparagraph, type of income, and tax rate percentage for each income type where the entity is eligible for treaty entitlement.

Please refer to the English website of the Korea Tax Authority for which article they are subject to when completing this section.

Country code

- Application for Entitlement to Reduced Tax Rate on Domestic Source Income (for Foreign Corporation), item 8;

- Application for Entitlement to Reduced Tax Rate on Domestic Source Income (for Non-resident Individual), item 6;

- Report of OIV, item 8;

- Schedule of BO, item 6.

{kind=link}

{kind=link}

{kind=link}

On the above forms and the mentioned items, please specify the two digit country code of the country of residency of the Applicant.

Please refer to the ISO website to retrieve the appropriate code.

Filing number

The filing number is the serial number assigned by the local tax withholding agent (Clearstream’s depository, The Hongkong and Shanghai Banking Corporation Limited, Seoul Branch (HSBC)) to register the forms accordingly. This section needs to be left blank by the Applicant as it will be our local depository who will complete this section upon receipt of the application form.

Filing date

The filing date is the date by which our local depository has received the application that has been completed by the Applicant. This section needs to be left blank as it will be our local depository who will complete this section upon receipt. This date inserted by our local depository is important because the tax form shall be valid for three (3) years from the filing date that will be inserted our local depository.

Signature section: Who should sign these documents?

The Applicant will need to sign and date the form in the applicable section.

For corporates, public OIV and OIV, the individual who represents the Applicant will need to sign and date the form in the applicable section.

According to the NTS, for funds, multiple parties such as the fund manager, trustee bank and distributors are involved. In such a case, based on the contractual agreement between the relevant parties, the Applicant should first identify who would be responsible for taxation for that fund, and after the identification process, it would be that representative who will need to sign the relevant tax document.

Attention “to” section

In this section, please mention the name of the local tax withholder, our depository: The Hongkong and Shanghai Banking Corporation Limited, Seoul Branch (HSBC).

Attorney-in-fact section

Attorney section should be completed when an attorney-in-fact submits the application form on behalf of the Applicant.

The Applicant could designate the attorney-in-fact as below:

- Tax administrator under Article 82 of the National Tax Basic Law: Only certified accounts or lawyers could be designated as tax administrator and the non-resident investors are required to report the designation to Korea tax authorities.

- Others: Anyone that does not apply in accordance with the above item (1) are required to submit the Power of Attorney together with a Korean translation.

Investment Registration Certificate

When the beneficial owner, OIV or Applicant is the holder of the Investment Registration Certificate (IRC), the name indicated in the IRC field must be the same name as mentioned in the IRC.

Korea is a beneficial owner market, which means that the IRC must be obtained in the name of the foreign investor who benefits from the Korean income. This rule is based on Article 6-10 of the Supervisory Regulation on Financial Investment Businesses enacted by the Financial Supervisory Commission, stating that the IRC must be obtained by the actual person who is the actual beneficial owner of the Korean income. The IRC must not be obtained in a shell/paper company name whose actual ownership of the Korean income vests in another person's name. In addition, omnibus accounts are not permitted in Korea.

Article 6-10 (the application of the Investment Registration Certificate)

- If a foreigner wishes to register with the financial supervisory service in order to invest in listed securities, the foreigner must file the investment registration certificate application form with official document(s) attached that proves its legal existence.

- If the foreigner applies in accordance to the above item (a), it shall be in the name of the person for whose account the investment will be made.

Responsibility of the Applicant

The Applicant is required to confirm on the tax forms that all information and attached documents provided are true and that the Applicant is the beneficial owner of all the domestic source income.

The Applicant should be aware that if any of the contents of this Application are different from true facts and/or the attached documents are submitted incorrectly, the local tax authorities can inquire further details. Based on the result of the investigation, the Korean tax authorities can issue a tax assessment bill retroactively for the past five (5) years.