Guide on completing the Report of Overseas Investment Vehicle (OIV) [Form No.29-13]

Definition of Overseas Investment Vehicle

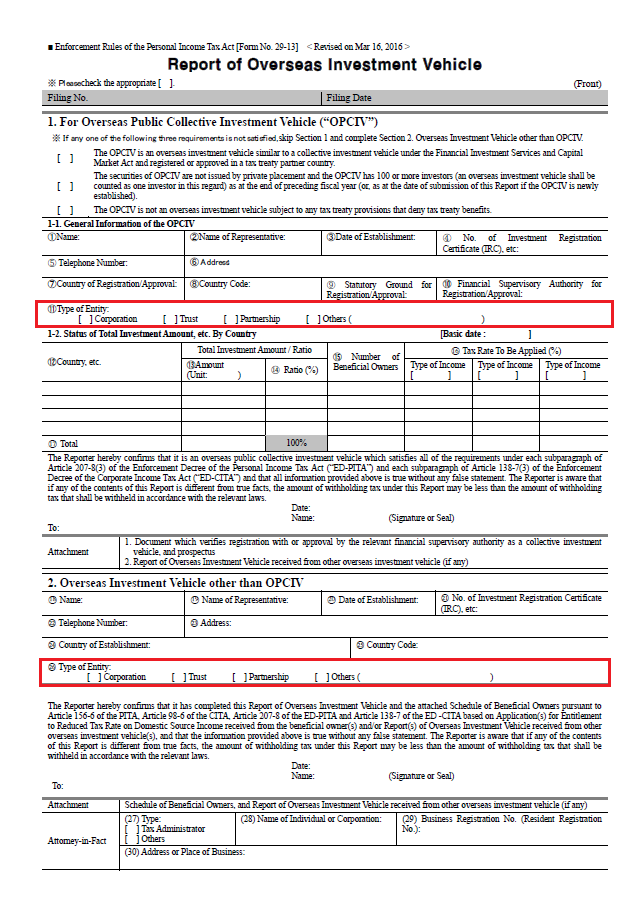

This form is intended for use by Overseas Investment Vehicles (OIV) or Public Overseas Investment Vehicles (OPCIV) defined as below.

The terminology OIV shall refer to an organisation that is established outside of Korea where it would solicit money from investors - and thereby manage the fund by investing in valuable assets including, but are not limited to, its purchases and sales of such assets - and distribute its profits to such investors. Partnerships, limited liability companies and other type of non-corporate type collective investment vehicles, for example, unit trusts, would likely be considered as an OIV. An OIV may also include a holding company vehicle owned by one or more investors.

Foreign investors which fall under the above definition must arrange to complete the Report of Overseas Investment Vehicle as opposed to the Application for Entitlement to Reduced Tax Rate on Domestic Source Income (for Foreign Corporation) [Form No. 72-2]. In case the fund is a corporate type fund, then please choose “corporation” and in case the fund is a trust type fund, please choose “trust” on Report of Overseas Investment Vehicle (OIV), items 11 and 26.

{kind=link}

Required Report of Overseas Investment Vehicle

OPCIVs who meet the three criteria explained below and provide the required proof documents, are eligible to provide only the status of total investment amount by country opposite to the disclosure of beneficial owners Schedule of Beneficial Owner. One condition is that the OPCIV should be established in the country where the tax treaty is concluded with Korea. Otherwise, it will be not treated as public OPCIV and will be required to complete the Schedule of Beneficial Owners.

Type of OIV | Country of establishment | Tax form required |

Non-public Overseas Investment Vehicle | In non-treaty countries | Report of Overseas Investment Vehicle (Section 2) Schedule of Beneficial Owner |

Public Overseas Investment Vehicle | In non-treaty countries | |

Non-public Overseas Investment Vehicle | In treaty countries | |

Public Overseas Investment Vehicle | In treaty countries | Report of Overseas Investment Vehicle (Section 1) with Status of total investment amount by country |

Additionally, if any of the underlying entities within the OPCIV are themselves an OIV, then a separate Report of Overseas Investment Vehicle is also required.

Public Overseas Investment Vehicle

Criteria for Public Overseas Investment Vehicle

OPCIV should meet all of the following criteria by selecting all three (3) boxes on Report of Overseas Investment Vehicle (OIV) For Overseas Public Collective Investment Vehicle (OPCIV) No.1 and also provide the required evidential documents.

{kind=link}

- The OIV should be an entity that is similar to a collective investment vehicle as defined in the financial and investment services and capital markets act and is registered or approved as per the law of its relevant country where there is a double taxation treaty with Korea.

- The OIV should not be offered as private placements and the number of beneficial owners within the OIV should be at least 100 as of the last day of the immediately preceding fiscal year (the OIV submission date for a newly established OIV). If the OIV is an investor of another OIV, the former OIV itself should only be counted as a single beneficial owner for the purpose of counting the number of beneficial owners.

- The OIV should not be defined as a non-tax treaty eligible entity in the relevant tax treaty.

What happens if there are less than 100 investors which make up the Public Overseas Investment Vehicle?

In the event that a OPCIV is unable to meet the minimum of 100 investors, then such OPCIV will not be permitted to complete the public OIV section of the Report of Overseas Investment Vehicle. One option investors can consider is to initially file under non-public OIV and then later revise to a public OIV (OPCIV) once after the fund has more than 100 investors. However, there are implications and investors should seek proper professional tax advice in this regard.

Required documents to be attached to the Report of Overseas Investment Vehicle

- A document which verifies their registration with, or approval by, the relevant financial supervisory authority of a country where there is a double taxation treaty with Korea as a collective investment vehicle.

- A prospectus, which serves to prove that the fund is distributed to the mass public. Korea tax authority would not acknowledge a trust deed unless the trust deed provides an article that the public fund is distributed to the mass public.

The above documents can be in English and in other foreign languages such as Japanese, Chinese, French or Spanish.

Status of total investment amount by country

The OPCIV is only entitled to treaty withholding rates in conjunction with the percentage of underlying beneficiaries that are entitled to treaty withholding rates. This information will be used by the local tax withholder, our depository, to utilise the average withholding rate on the OIV’s Korean sourced income.

Below is an example of how this section would need to be completed on the Report of Overseas Investment Vehicle, Status of total investment amount, etc. by country, No.1-2.

{kind=link}

12 Country, etc. | Total Investment Amount / Ratio | 15 Number of Beneficial Owners | 16 Tax Rate To Be Applied (%) | |||

13 Amount (Unit: KRW ) | 14 Ratio (%) | Type of Income [Interest from cash balances ] | Type of Income [Dividend] | Type of Income [Interest from bonds] | ||

Canada | KRW 301,234 | 30.1234% | 3,044 | 10% | 15% | 10% |

United States | KRW 209,000 | 20.9000% | 1,234 | 13.2% | 16.5% | 13.2% |

United Kingdom | KRW 191,0000 | 19.1000% | 4,344 | 10% | 15% | 10% |

ZZ | KRW 298,766 | 29.8766% | 45,00 | 22% | 22% | 15.4% |

17 Total | KRW 1,000,000 | 100% | 53,622 | 14.2540% (Sum of 3.0123%+2.7588%+ | 17.4049% (Sum of | 12.2821% (Sum of |

To obtain the average withholding rate, the investment ratio under section (14) should be multiplied with the tax rate under section (16). Thereafter, please provide the sum of all tax rates under the row total (17).

Percentage rate needs to be rounded up at the fifth digit and the foreign investor needs to quote up to 4 digits in percentage points. In the above example, for the United States on interest from cash balances, 13.2% multiplied by 20.9000% is 2.7588%. Please round this up to the fifth digit and the figure will be 2.7588%. The same process needs to be done for Canada, United Kingdom and ZZ which is the default tax rate. Please then add all the tax rates per each country to obtain the average tax rate applicable to the whole fund.

As a result, the applicable average tax rate for the fund will be as follows:

- 14.2540% for interest on cash balances;

- 17.4049% for dividend; and

- 12.2821% for interest from bonds.

Public Overseas Investment Vehicle - How frequently is Public Overseas Investment Vehicle required to submit the Overseas Investment Vehicle report?

The tax form will need to be submitted where it classifies the beneficial owners by each country at the time of submitting the Report. The Korea Tax Authority has explained that the composition of unit holders of a public fund can change on a daily basis, therefore, in principle the report would need to be resubmitted on a daily basis. If, however, it is considerably difficult to resubmit the Report, the Korea Tax Authority explained that the report can be prepared and be submitted by using the information as at the end of the preceding half-year from which the Report is submitted (the Report can be submitted once every half-year) or the status of investors can be based on any date going backwards within 6 calendar months from the date of income payment date.

The following is an example of the validity of the report submitted by a OPCIV in cases where the report is submitted on a quarterly basis in order to continue to enjoy the reduced tax rate:

| Base date a | Period applicable to reduced treaty rate |

| For the form as of 30 June | from filing date to 31 December |

| For the form as of 31 December | from filing date to 30 June of the following year |

--------------------

a. Base date: The Applicant needs to declare the status of investors, that is, section 1-2 of the OIV report - Status of Total Investment Amount, etc by country.

The default tax rate will be applied after each base date until the revised tax form is filed in, if there is any income payment between the base date and the revised filing date.

Name of Investment Registration Certificate

If the OIV is the holder of the Investment Registration Certificate (IRC), the name indicated in the IRC field must be the same as mentioned in the IRC.

For a fund, several entities are generally involved such as Fund, Fund manager, Trustee bank, Distributor, Global Custodian bank, Sub-custodian bank or Unit Holder. In such case, the Financial Supervisory Service has explained that the IRC must be obtained in the name of the fund.

Note: For Sub-Funds or Parent-Funds, in which name should the IRC be obtained?

Due to the Financial Supervisory Service regulations, if there are many multiple sub-funds under a parent-fund, and if the beneficial owner of the Korean income from the investment by the sub-funds rests (vests) under the parent-fund, then the IRC must be applied in the name of the parent-fund. However, if the beneficial owner of the Korean income from the investment by the sub-funds vests in each of the sub-fund, then the IRC must be applied in the name of each sub-fund.